Market reports indicate the global medical device industry for Q3 2024 saw an increase in merger and acquisition (M&A) activity in terms of value year-over-year. Although deal value decreased compared to Q2 2024, deal volume increased compared to Q2 2024 and year-over-year. One report states there were 168 medical device M&A deals announced in Q3 2024, worth a total value of $14.4B. For the global medical devices market, GlobalData reports the following for Q3 2024:

- global medical devices deals worth $34B – an increase of 25% compared to Q3 2023

- 275 M&A deals – an increase of 35% compared to Q3 2023

- 8 mega-deals (valued at more than $1B) – an increase of 14% compared to Q3 2023

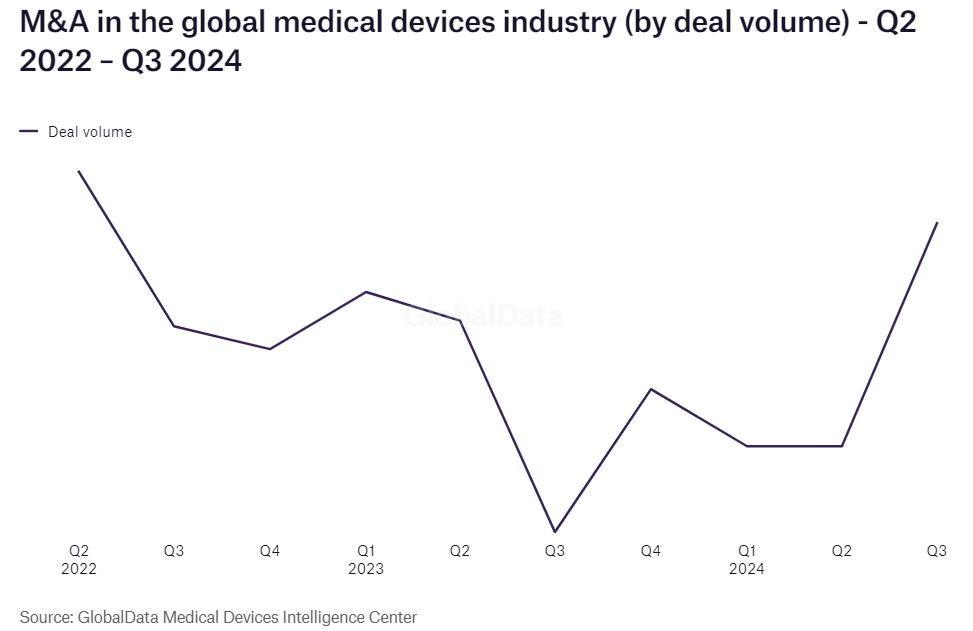

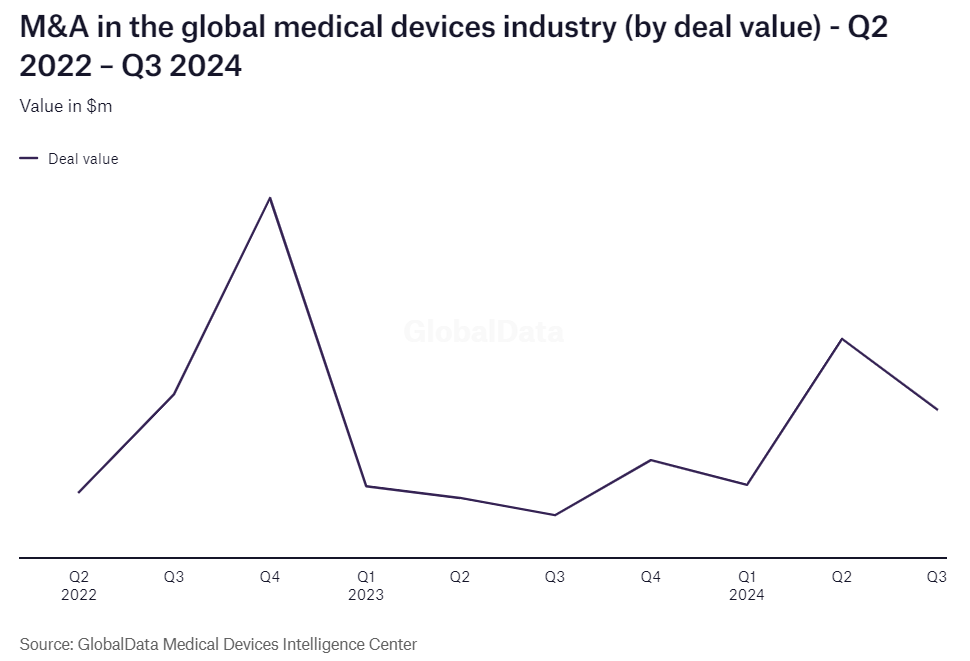

The Medical Device Network shows the following qualitative charts from GlobalData for global medical device deal volume and deal value from Q2 2022 to Q3 2024:

According to GlobalData, the largest medical device M&A deal by value since Q1 2023 is the Carlyle Group asset transaction with target Baxter International – Vantive Kidney Care for $3.8B (Q3, 2024). The remaining top four medical device deals by value since Q1 2023 are the following:

- Becton Dickinson and Co. in an asset transaction with target Critical Care for $4.2B (Q2, 2024)

- Merger of Globus Medical and NuVasive valued at $3.752B (Q1, 2023)

- Thermo Fisher Scientific acquires Olink Holding for $3.1B (Q4, 2023)

- J&J acquires Shockwave Medical for $1.31B (Q3, 2024)

In the related “medtech” sector, Goodwin reports the sector “is heading toward 2025 with solid momentum.” J.P Morgan reports that in medtech, as of Q3 2024, “M&A activity has already passed prior years in the number of deals with the dollar totals ready to pass as well.” In particular, “2024 YTD has seen 195 medtech acquisitions totaling $47.0 billion. In FY 2023, 128 medtech M&A deals were announced, totaling over $50.1 billion.” J.P. Morgan further reports that venture investment activity in medtech in 2024 “through the third quarter is set to beat full-year 2023 activity.” For example, “medtech venture activity through Q3 2024 has seen $16.1 billion from 554 funding rounds. Venture investments during the third quarter of 2024 totaled $5.1 billion across 154 rounds, up approximately $1 billion compared to Q3 2023.”

In the “healthcare” sector, Leerlink Partners reports that M&A activity “increased in the third quarter of 2024, with 33 transactions vs. 21 in 2023.” Within the healthcare sector generally, “healthcare services was the most active healthcare subsector, representing 42% of deal volume, with the most notable transaction being TowerBrook’s and CD&R’s $8.3B acquisition of R1 RCM.”